ING Authors Carsten Brzeski and James Smith map out the hit to the global economy and possible path for recovery under four different Covid-19 scenarios

While quarantining and social distancing is the right prescription to combat COVID-19’s public health impact, the exact contrary is needed when it comes to securing the global economy. Economic contagion is now spreading as fast as the disease itself. As more countries impose quarantines and social distancing, the fear of infection and income losses is increasing uncertainty around the world.

Governments are considering and rolling out large incentive packages to prevent a sharp downturn of their economies which could potentially drop the global economy into a deep recession. Early estimates predicated that, should the virus become a global pandemic, most major economies will lose at least 2.4 percent of the value their gross domestic product (GDP) over 2020, leading economists to already reduce their 2020 forecasts of global economic growth down from around 3.0 percent to 2.4 percent. In the worst-case scenario, the world economy could contract by 0.9 per cent in 2020.

The 4 Economic Scenarios out of Covid 19

The scenarios below that the interplay between the virus and society’s response might reveal and the implications on the economy in each case. At ING, they have developed four scenarios of how the virus, the lockdown measures and consequently the different economies could progress. Unnecessary to say, even these scenarios cannot try to fully predict reality, but we hope they can provide a benchmark for both the extremes and the middle-ground. In each case, we have laid out some possible health factors that may be driving the scenarios although we would highlight these are not meant to be interpreted as forecasts.

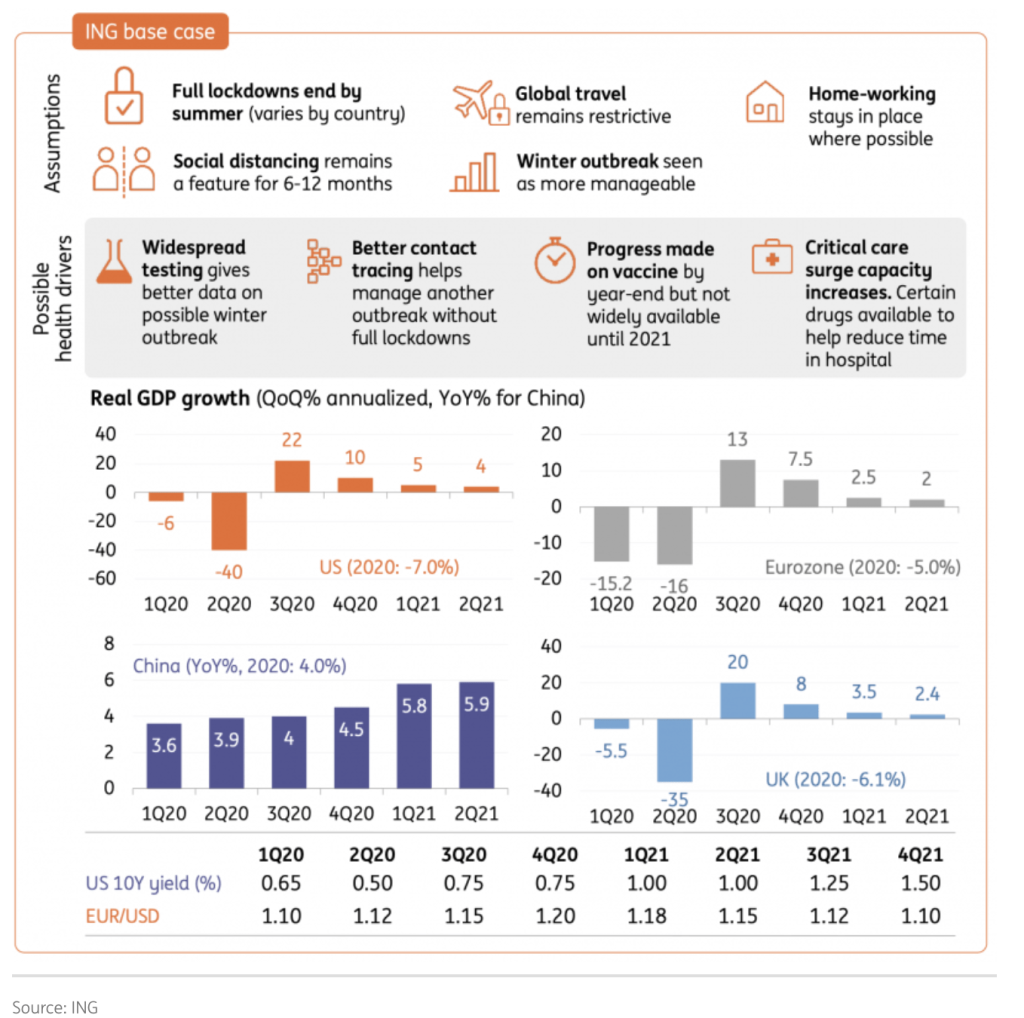

Scenario 1: Base case

In this scenario, the experts have discussed the base case of COVID-19 and the main purpose of this scenario for the major economies as well as their latest monthly updates. Growing limitations on the movement of people and lockdowns in Europe and North America are hitting the service sector hard, particularly industries that involve physical interactions such as retail trade, leisure and hospitality, recreation and transportation services. Collectively, they account for more than a quarter of all jobs in these economies. As businesses lose revenue, unemployment is likely to increase abruptly, transforming a supply-side shock to a wider demand-side shock for the economy.

The adverse effects of extended restrictions on economic activities in developed economies will soon spill over to developing countries via trade and investment channels. The COVID-19 pandemic will not only defeat economic growth, it will also badly impact sustainable development in the short run.

In Africa, an outbreak of the virus is of extreme concern because of the fragility of countries’ healthcare systems and because many of these economies already face significant public health challenges, particularly malaria, measles, HIV, and tuberculosis. During the 2014–16 Ebola outbreak, many of the deaths were due to resources being diverted away from other diseases.

In Western Asia, the pandemic is likely to impact humanitarian action of the international community in Iraq, Syria and Yemen, where ongoing conflict still requires timely responses. The return to normality is gradual, and social distancing continues for at least the entire summer. As a result, Economic recovery will be U-shaped but still most countries will experience a more severe contraction of economic activity than during the financial crisis.

Scenario one at a glance

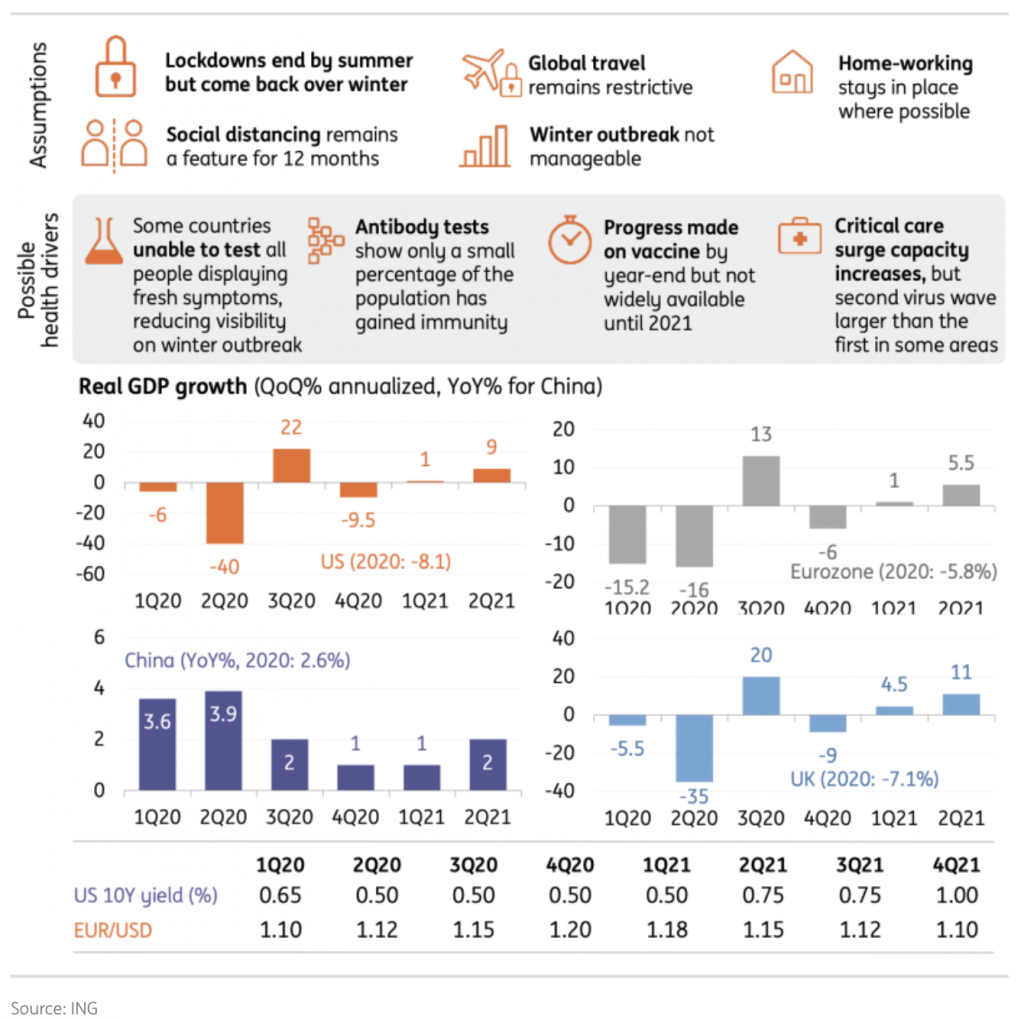

Scenario 2: Winter lockdowns return

This is a slight similarity of the aforementioned base case scenario. Lockdown end by summer but come back overwinter. It starts off in much the same way, with a gradual easing of lockdown measures in May and June as delayed testing and weak adoption of social distancing stymie the public-health response. The virus does not prove to be seasonal, leading to a long tail of cases through the rest of the year. Africa, Oceania, and some Asian countries also experience widespread epidemics, though countries with younger populations experience fewer deaths in percentage terms. Even countries that have been successful in controlling the epidemic (such as China) are forced to keep some public-health measures in place to prevent revival.

“For indicative purposes, we’re assuming it will take until April 2021 before the virus is back under control and economies, as well as societies, begin to return to normality. This is a ‘W-shaped recovery’,” the experts said. Winter lock down return impact would be severe, approaching the global financial crisis of 2008-2009. GDP contracts significantly in most major economies in 2020 and recovery begin only in 2021. Some countries unable to test all the people showing fresh symptoms reducing visibility on winter break. Antibodies shows only a small percentage of the population has gained the immunity. Critical case surge capacity increases, but second virus wave larger than the first in some areas.

Scenario two at a glance

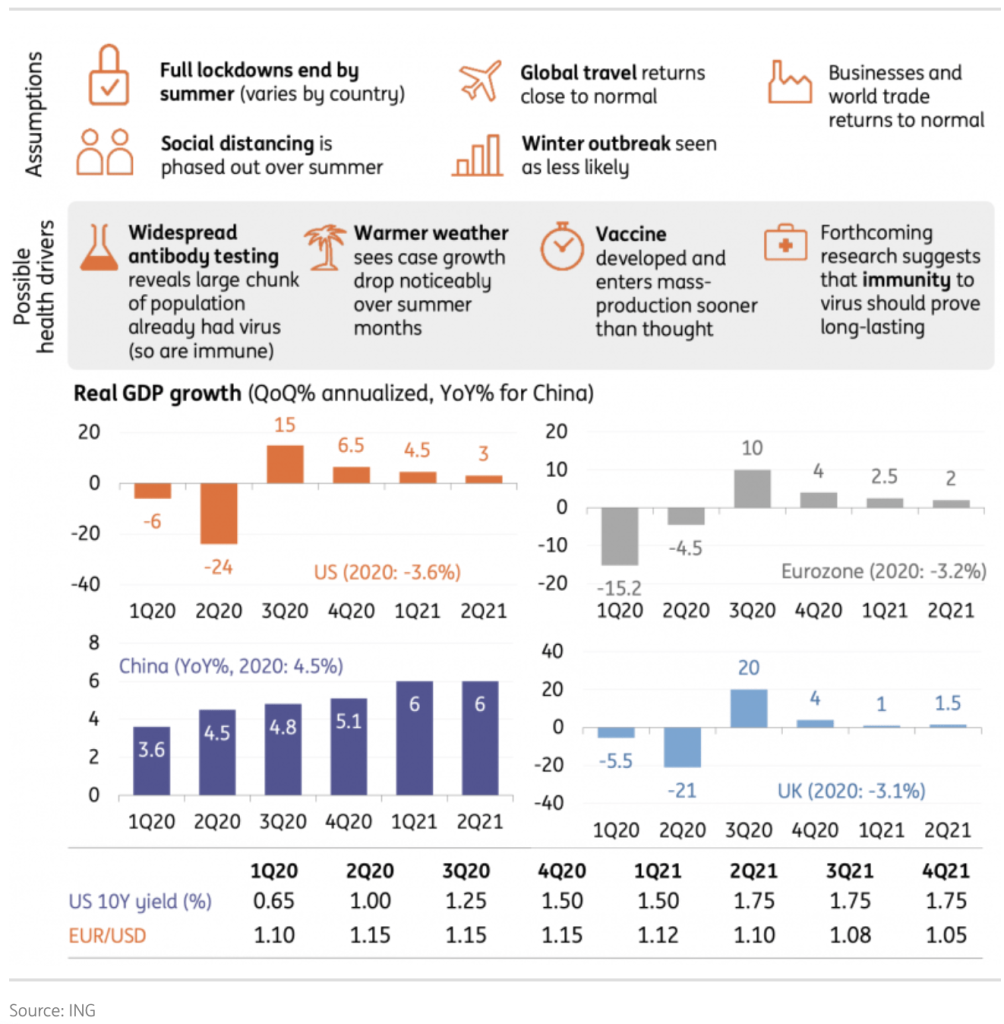

Scenario 3: The ‘best’ case

In the best-case scenario, the western world follows the techniques of China by ending the lockdown as well as the outbreak of the COVID-19. A quick return to the normal condition is expected for the end of April. In this scenario, the experts also consider that the virus does not back again in the winter because larger volume of infected people of Covid-19 had the virus and built a strong immunity system, making control measures much more effective. Fewer people will be infected because the effects of the control measures, but it’s too early to tell whether efforts to quarantine people, and the widespread use of face masks, are working.

With moderate failures in private consumption, investment and exports and offsetting increases in government spending in the G-7 countries and China global growth would fall to 1.2 per cent in 2020. Government measures like guarantees, liquidity support and short-time work schemes foster a quick and strong rebound, nevertheless some differences across countries depending on when the lockdown measures end.

This is effectively a ‘v-shaped’ recovery scenario. In this scenario, most economies would experience a slight downturn of some 2-3% year-on-year but growth in 2021 would accelerate, returning most economies to their pre-crisis levels. Business and world trades returns to normal. Full lockdown end by summer differs by every country. Widespread of antibody testing exposes large chunk of population already had a virus. Social distancing is faced out over summer. Upcoming research suggests that immunity to virus should prove long-lasting.

Scenario three at a glance

Scenario 4: The ‘worst’ case

The worst case in Covid-19, lockdowns remain largely in place until year end. Things return to normal from 2021. If the vaccines are developed and able to deployed over the winter months the recovery here may be a little faster and stronger than in the other scenarios, as the virus is assumed to be completely under control. This is an ‘L-shaped’ recovery. As the experts pointed out: “Needless to say, this is an extreme scenario with lots of economic, social and political turmoil, and one that looks pretty unlikely at this stage.

In this scenario, most economies would experience an unprecedented and almost unimaginable contraction in 2Q20 of around 50% quarter-on-quarter annualised. The year 2020 would go down in the history books as the year with the most severe recession on record, seeing most economies shrinking at double-digit rates for the year as a whole.”

Scenario four at a glance

ING experts believe in a minor possibility that the world will get away with a shock. However, this is rather unlikely. They rather believe that we have to prepare for a distinct and prolonged recession. This means we will be seeing a sharp drawdown in economic activity and the financial markets, which have already started to price this scenario as the main scenario as well. The coronavirus crisis is a story with an unclear ending. What is clear is that the human impact is already tragic, and that companies have an imperative to act immediately to protect their employees, address business challenges and risks, and help to mitigate the outbreak in whatever ways they can.

These scenarios are only a starting point for conducting a more detailed analysis based on the particular conditions of different locations. But the data make one thing clear; if companies and hospitals tie their futures to a strategy based on one potential scenario, they might miss the mark by an order of magnitude. The richer the understanding of the possibilities, the less destabilizing the outbreak will be and the sooner life can begin to get back to normal.

Simon Pearson is an independent financial innovation, fintech, asset management, investment trading researcher and writer in the website blog simonpearson.net.

Simon Pearson is finishing his new book Financial Innovation 360. In this upcoming book, he describes the 360 impact of financial innovation and Fintech in the financial world. The book researches how the 4IR digital transformation revolution is changing the financial industry with mobile APP new payment solutions, AI chatbots and data learning, open APIs, blockchain digital assets new possibilities and 5G technologies among others. These technologies are changing the face of finance, trading and investment industries in building a new financial digital ID driven world of value.

Simon Pearson believes that as a result of the emerging innovation we will have increasing disruption and different velocities in financial services. Financial clubs and communities will lead the new emergent financial markets. The upcoming emergence of a financial ecosystem interlinked and divided at the same time by geopolitics will create increasing digital-driven value, new emerging community fintech club banks, stock exchanges creating elite ecosystems, trading houses having to become schools of investment and trading. Simon Pearson believes particular in continuous learning, education and close digital and offline clubs driving the world financial ecosystem and economy divided in increasing digital velocities and geopolitics/populism as at the same time the world population gets older and countries, central banks face the biggest challenge with the present and future of money and finance.

Simon Pearson has studied financial markets for over 20 years and is particularly interested in how to use research, education and digital innovation tools to increase value creation and preservation of wealth and at the same time create value. He trades and invests and loves to learn and look at trends and best ways to innovate in financial markets 360.

Simon Pearson is a prolific writer of articles and research for a variety of organisations including the hedgethink.com. He has a Medium profile, is on twitter https://twitter.com/simonpearson

Simon Pearson writing generally takes two forms – opinion pieces and research papers. His first book Financial Innovation 360 will come in 2020.

{kind=link}