When it comes to establishing a hedge fund, start-up managers need to have a firm understanding of the legal issues affecting hedge funds in order to get things right from the start.

This guide will help you get to grips with the legal issues you need to consider when deciding how best to structure your fund and its management.

Hedge Fund Structures

First things first, there is no one-size-fits-all hedge fund structure. It really needs to be tailored to suit the start-up managers vision of the fund-raising process, and where investors will be based. Considerations such as: will this be a targeted EU-only strategy, or will this be a global aimed at a range of investors worldwide, need to be taken into account.

Common Hedge Fund Structures:

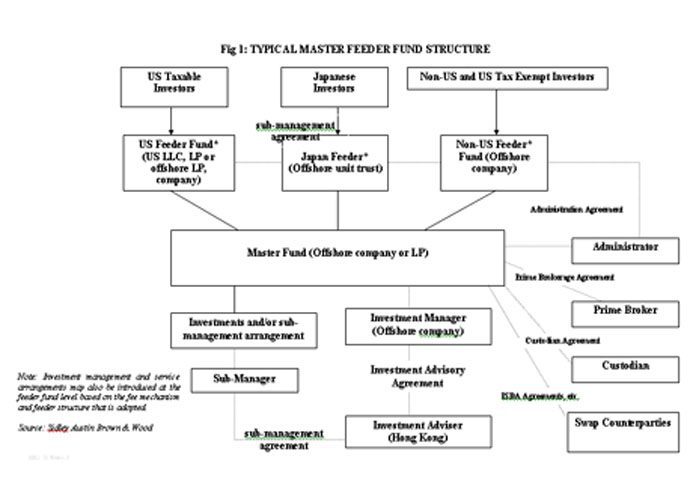

Cayman Master/Feeder structure

Source: Eurekahedge.com

The vast majority of fund managers tend to aim towards raising money from both EU institutions and US tax payers and US tax-exempt investors. In this case, the common Cayman master/feeder structure is often the best way forward.

In simple terms, US investors can basically be split into two categories: investors who are US tax-exempt and investors who are US tax payers.

Investors who pay tax will generally want to be taxed as if they were holding the underlying assets directly in a tax-transparent structure. Those that do not pay tax will tend to want a tax-opaque structure where they are taxed on the returns generated in the fund vehicle.

So we have a conundrum here, ie, tax-transparent or tax-opaque? Within given limits, any legal vehicle can decide how its going to be classified for US tax purposes. However, its obviously impossible to set up a fund thats both tax-transparent and tax-opaque.

In this case, its the role of the fund manager to do is set up a minimum of two vehicles to support these two different types of investor. These are referred to as feeder funds.

The manager also needs to establish a third structure – the master fund. The separate feeder funds provide multiple entry points into the master fund, which exists to hold the assets. All trades that are carried out with the prime broker(s) are done so within this master fund.

In this classic dual-legged set up, one feeder fund is a Cayman Islands company that support the funds US tax-exempt investors, while the other is a tax-opaque Delaware limited partnership, which supports the US taxpaying investors. Both feed the master fund, which is typically a tax-transparent Cayman company.

The Dechert Model

Managers in this situation might also consider a second common option, which gets rid of the need for the double-layer of transparency. The Dechert Model instead uses a single-legged master/feeder structure.

The reason for this set up is that it allows you to bring investors straight into a transparent master fund. Basically, here you create a single Cayman partnership with a single Cayman corporate, for US tax-exempt investors, feeding into it.

The benefit of this Dechert Model is that investors save in set-up costs as theres not Delaware Partnership to worry about. However, some investors may be put off this model when they want to keep their US taxpaying investors completely separate from the rest of their global tax-paying investors for accounting purposes, and also simply because the Delaware LP is the most common hedge fund structure in the US market.

Other articles in this series:

- Structuring a Hedge Fund and Fund Management Company: The Legal Issues – Part Two

- Structuring a Hedge Fund and Fund Management Company: The Legal Issues – Part Three

I am a writer based in London, specialising in finance, trading, investment, and forex. Aside from the articles and content I write for IntelligentHQ, I also write for euroinvestor.com, and I have also written educational trading and investment guides for various websites including tradingquarter.com. Before specialising in finance, I worked as a writer for various digital marketing firms, specialising in online SEO-friendly content. I grew up in Aberdeen, Scotland, and I have an MA in English Literature from the University of Glasgow and I am a lead musician in a band. You can find me on twitter @pmilne100.

{kind=link}